Customer experience (CX) is the defining competitive differentiator in the banking industry today, and for good reason: Financial institutions that invest in the customer experience in banking have higher rates of recommendation, greater wallet share, and are more likely to up-sell or cross-sell products and services to existing customers.

This has incentivized banks, credit unions, and other financial institutions around the globe to take a more discerning look at their current products and services to determine whether there’s room to provide a greater degree of customer-centricity and personalization to enhance the financial services customer experience.

Looking to make some changes to your institution? We’ve compiled this list of top banking customer experience trends for 2023 to help you get started.

What Is Customer Experience in Banking?

As its name implies, customer experience in banking refers to a customer’s collective experience interacting with various touchpoints, including online banking systems, emails, call centers, online advertising, face-to-face interactions, and even social media.

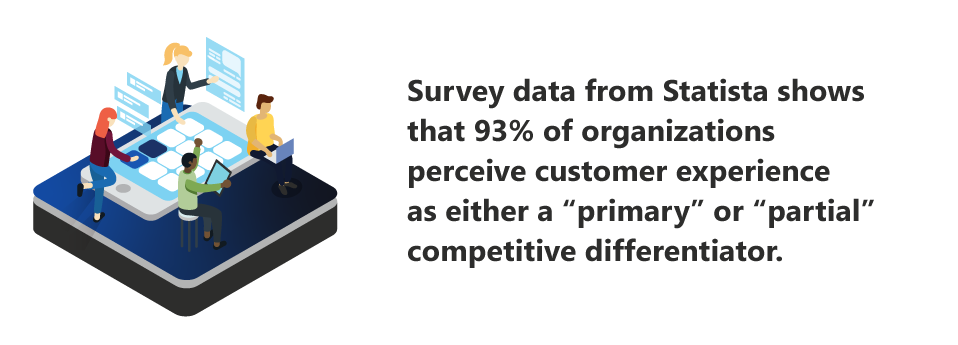

The customer experience in banking is important for two key reasons: First, CX is a critical marketing battlefront. Survey data from Statista shows that 93% of organizations perceive customer experience as either a “primary” or “partial” competitive differentiator. Second, the better a customer’s experience, the more likely they are to remain loyal to a brand or institution, meaning CX has the power to improve customer retention.

State of the Industry

Before we explore the biggest banking customer experience trends for 2023, let’s first contextualize them by taking a look at what’s happening within the financial services industry. Over the past year, we’ve seen many changes within this space, with new priorities emerging. These include:

- Smart, savvy fintech competitors have entered the market, disrupting traditional customer relationships.

- Global digitization has changed customer expectations to include 24/7 self-service, lightning-fast response, and personalized experience across service channels and payment platforms.

- With sophisticated cybercrime on the rise, maintaining security and privacy are critical to customer trust.

- Stringent and complex regulatory compliance must be maintained to ensure a good reputation and avoid security breaches, fines, and litigation.

- Spending cuts and shrinking budgets hinder the ability to properly maintain IT infrastructures properly, leaving them vulnerable and potentially impairing customer service.

- Faced with rising consumer expectations and a disruptive economy, many banks have dropped the ball with customer experience and now find themselves at an inflection point.

12 Trends Reshaping Customer Experience in Banking for 2023

1. Enhancing Products & Services with Mobile App Data

Customer self-service is one of the fastest-growing banking customer experience trends. Thanks to mobility, customers now have the ability to fully access their bank’s resources from their mobile device anywhere they have Wi-Fi, turning what was once a distant dream into a basic expectation.

In today’s market, mobile banking applications aren’t so much a nice-to-have as a need-to-have, and banks without this capability are at a severe disadvantage because customers have come to expect the unparalleled convenience a mobile app provides. The good news is that these apps are easy enough to develop, either through the use of a low-code development platform or in partnership with a vendor.

If your institution already has a mobile banking app or recently developed one, the next step is to determine whether you’re utilizing the data from that app effectively. Mobile applications collect a massive amount of data — data that doesn’t do you or your customers any good when it’s left untouched. Data analytics platforms and machine learning algorithms can help you extract valuable information from this customer data, which you can then leverage to develop new products, optimize existing processes, better empower customers, and improve the overall CX.

2. The Branch of the Future

Customers might not visit physical branches as frequently as they once did, but that doesn’t mean banks can afford to sleep on their brick-and-mortar locations. Most brick-and-mortar banks recognized early on that internet banking presented a risk to their model, that small perks such as complimentary coffee and Wi-Fi aren’t enough of a draw for modern customers, and that their physical branches will be shut down if they fail to turn a profit.

The need to compete with internet banks and to improve the customer experience in banking has driven brick-and-mortar banks to reimagine what a physical branch can be and what the “branch of the future” should look like. Some banks have experimented with a showroom-style design similar to that found in Apple Stores, with rows of smartphones and other mobile devices loaded up with their banking app on display, so customers can see the app in action.

Others have capitalized on the value of one-on-one, face-to-face interactions by turning their physical branches into customer training venues, where customers can seek consultative services and learn how to use technology to make their money go the extra mile.

Ideally, the branch of the future should offer both of these functionalities, as well as self-service options, community space, and advanced technology so that each customer can have a hyper-personalized banking experience that is specific to their unique needs.

3. Advising Services

Most banking customers are looking for ways to grow their money but aren’t sure where to begin; those who turn to the internet for guidance will likely find the advice on financial sites to be informative, but too broad to be of any real use. This gives banks the perfect opportunity to improve the financial services customer experience by pairing consumers with in-house financial advisors who can provide guidance tailored to each customer’s needs.

With customer relationship management (CRM) technology, you can collect and analyze data and build detailed customer profiles, which your in-house advisors can then use to gain a 360-degree view of the customer and their unique situation. This level of insight is incredibly valuable because it enables advisors to offer personalized advice for customers at every stage of their financial journey, build stronger customer relationships, and ensure customer loyalty.

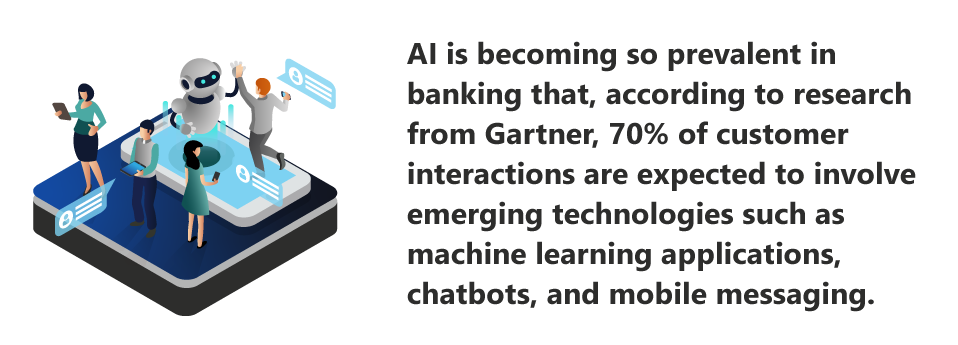

4. Artificial Intelligence

There’s nothing more frustrating to a customer than calling their bank’s customer service helpline to report an issue, only to be put on hold. With the volume of incoming calls steadily increasing and not enough representatives on hand to field them, it’s becoming a fraught situation for financial institution call centers.

Fortunately, with customer self-service becoming increasingly popular, innovative solutions are being developed to alleviate this strain and to improve the customer experience in banking. Rather than wait on the phone, customers now have the option to consult AI-enabled chatbots when faced with challenges.

These chatbots pull and process information from various sources, such as the bank’s knowledge base and CRM customer profiles, to respond to incoming customer service requests. Should a particular request exceed the chatbot’s capabilities, it’s automatically escalated to a live service representative who can help the customer work toward a resolution.

Best of all, more and more banking apps are offering chatbot technology as a native functionality, which means customers can quickly resolve issues from anywhere, at any time.

Banks and their customers both stand to gain from AI innovation: Customers no longer have to waste valuable time waiting to talk to a representative, while banks stand to save a substantial number of resources that would be otherwise funneled to their call centers. Some financial institutions have even used AI to improve the customer experience in banking even further by developing AI-enabled virtual assistants to provide money management tips and tricks.

5. Automated Onboarding

A quality customer experience hinges on a good first impression; for most banking customers, that first impression takes place during onboarding. Traditionally, new customer onboarding involves filling out and signing stacks of paper, which places an administrative burden on onboarding teams and increases the risk of process bottlenecks, testing customers’ patience.

By making onboarding an electronic process rather than a manual, paper-based one, banks make it easy for their customers to provide essential onboarding information from the comfort of their own home. From there, banks can use automation to expedite key parts of the process, so customers can open their accounts much faster, further enhancing the overall CX.

6. Support for Digitalization & Remote Service

If there’s one thing the past few years have taught us, it’s the importance of digital channels and remote services. The COVID-19 pandemic prompted businesses across all industries to expand their remote offerings — a concerted effort that not only enhanced public safety at the height of the pandemic but also improved access for people with disabilities, thereby allowing for more inclusive customer experiences. That said, making the transition to digital has proven difficult for many banking customers, especially older generations that possess limited digital literacy.

Rather than let these customers simply fall to the wayside, in 2023, banks will need to redouble their efforts to smooth the transition to online banking services. This will require banks to provide customers with additional support in the form of educational content, such as step-by-step tutorials, interactive videos and webinars, customer knowledge bases, and more.

The more comfortable and confident a customer feels interacting with digital channels and remote services, the better their overall financial services customer experience will be.

7. “Humanizing” Digital

Although AI and digital channels are both leading banking customer experience trends for 2023, there’s still something to be said for the value of human interaction. To that end, a growing number of banks offer a mix of AI and live support for customer service, generating efficiency gains while still providing customers with the kind of personal touch they crave.

Some financial institutions have taken this concept a step further, experimenting with different methods to make their chatbots and other AI services feel more human; examples include giving chatbots personalities, using customized conversation openings, and leveraging sentiment analysis to detect emotion and respond appropriately.

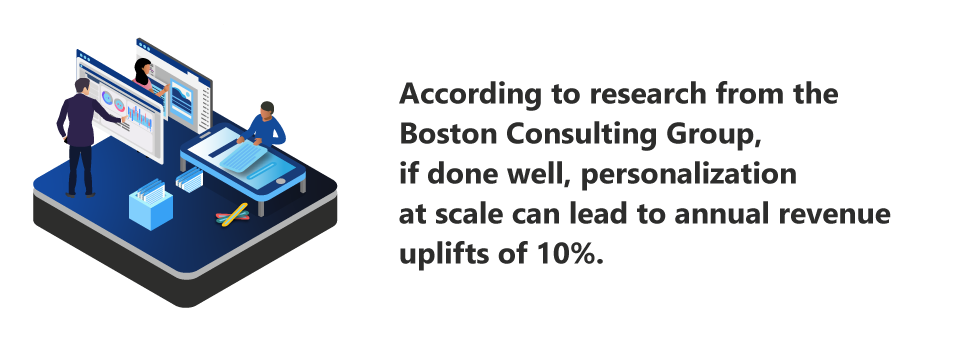

8. Hyper-personalization

It’s no secret that personalization is important to banking customers — after all, it’s been topping CX trends lists for years. And banks benefit, too: According to research from the Boston Consulting Group, if done well, personalization at scale can lead to annual revenue uplifts of 10%.

As we enter 2023, we can expect to see financial institutions — especially neobanks — placing heavy emphasis on hyper-personalization. Compared to standard personalization, which uses data analytics to deliver targeted marketing and sales messaging to different customer segments, hyper-personalization drills down to the individual customer.

Banks can achieve hyper-personalization by using a combination of predictive analytics, AI, and machine learning to monitor individual customers’ real-time usage data, such as which phrases they commonly search, what content they like to view, their geographic location, and so on.

Armed with this information, banks can queue more targeted, one-to-one marketing campaigns and offers. For example, if search data revealed that a customer frequently searched the terms “homes for sale in my area,” “how to apply for a home loan,” and “mortgage rates 2023,” you might reasonably presume that the customer was looking to purchase a home and was, therefore, a good candidate for a home loan.

Based on that information, you might target that customer with an offer for a home loan with a low-interest rate. If that particular customer was in good financial standing with a solid credit score, you might even reach out to them about prequalifying for a home loan.

9. Greater Transparency Around Data Usage

In order to engage in the kind of micro-segmentation necessary for hyper-personalization, banks must collect and analyze large quantities of customer data. But it isn’t enough just to gather this data — banks need to secure it, as well. Recent cybersecurity incidents within the financial services sector, such as the 2019 Capital One data breach and the 2020 Experian data breach, have made consumers understandably wary of how institutions handle their data.

According to research from KPMG:

- 86% of consumers say that data privacy is a growing concern for them

- 68% are concerned about the level of data being collected by businesses

- 40% don’t trust companies to ethically use their data

- 30% aren’t willing to share their personal data for any reason

To prevent distrust from souring the financial customer experience, banks must make every effort to be transparent with their customers about how they process, use, and secure personal data. Not only is being open and honest about your data policies and practices an easy way to show goodwill and earn trust, it’s also a requirement for certain regulations, including the General Data Protection Regulation and the California Consumer Privacy Act.

In addition to being more transparent about their data practices, banks should also look to prioritize zero-party data — that is, data that customers readily volunteer — over third-party and even first-party data. Though it can be harder to collect, zero-party data is typically more accurate and offers banks direct insight into how their customers think, feel, and behave. You can incentivize customers to share zero-party data by offering rewards and discounts in exchange for personal information.

10. Proactive Engagement

One of the beautiful things about advanced analytics is that it provides financial institutions with a level of insight into their customers that once seemed impossible. Now, banks can monitor customers’ financial health and proactively offer assistance with financial management or suggest opportunities to grow their wealth.

This type of proactive engagement can take place across any number of channels — in-person, over the phone, through their banking app, via email, and so on — depending on each customer’s personal preference. We can expect to see more banks going above and beyond in 2023 to watch out for the interests of their customers in order to demonstrate the value they add and enhance the overall financial services customer experience.

11. Embedded Banking

Customer journeys in the financial services sector should be designed in such a way that they minimize consumer effort; embedded banking is an effective way to achieve this.

Embedded banking — also known as embedded finance — is a form of Banking as a Service, in which banks white-label their services for use by non-financial companies, particularly retailers. Non-financial companies will then build these banking services directly into their purchasing process, creating a contextual, seamless shopping experience for customers.

One of the most prominent examples of embedded banking is the Starbucks app, which enables customers to save their payment details directly within the app and make on-click purchases. Buy now, pay later platforms such as Klarna and Afterpay, which enable shoppers to finance purchases through installment loans, are another common example.

Research from Bain & Company shows that embedded finance accounted for $2.6 trillion, or 5%, of total U.S. financial transactions in 2021; that figure is expected to exceed $7 trillion by 2026. FinTechs have been the primary driver behind this growth, but the window of opportunity is closing for traditional financial institutions to get in on the game. By investing in the right technical capabilities and carefully assessing vertical segments, incumbent banks can form smart partnerships that generate new growth opportunities and streamline the banking customer experience.

12. Doing the Right Thing

As we come out of what has been an exceedingly challenging year — one that has caused significant financial hardship for many households — it’s vital that banks make even more of an effort to do right by their customers in 2023.

A good place to start is by reevaluating your institution’s marketing strategy so that you only target customers with products and services that actually align with their needs and goals; hyper-personalization plays a major role in this. And circling back to advising services, they can be a great way to increase customers’ financial literacy and improve their financial health, enabling them to regain their footing after a fraught year.

There are other small ways for banks to show that they care about customers’ long-term well-being, from delivering custom alerts to help consumers stay on top of payments to offering guidance on how to avoid fees. Ultimately, doing the right thing is all about demonstrating to customers that you intend to put their best interests first — whatever that might look like.

And if banks are looking for an incentive to do right by their customers beyond the satisfaction of a job well done, consider these data points from J.D. Power:

“Overall customer satisfaction with retail banks rises 155 points (on a 1,000-point scale) when customers cite that their bank supports them during challenging economic times. Similarly, 63% of customers say they definitely will not switch banks and 78% say they definitely will reuse their bank when it delivers this support.”

5 Examples of Banks with Outstanding CX

Interested in seeing examples of banks that really get financial services customer experience right? Look to these five for inspiration:

- JPMorgan Chase: The largest bank in terms of asset share in the United States, Chase earns high marks for its comprehensive and easy-to-use mobile banking app, rapid customer service, and free online bill payment system. The company recently debuted a new online educational video series, Hart of It All, in which comedian Kevin Hart helps actual Chase customers shape their financial futures through a series of fun and engaging challenges. Chase has received numerous awards and recognitions for its customer service and consistently sits at or near the top of J.D. Power rankings for customer satisfaction.

- TD Bank: There’s a reason why TD Bank refers to itself as “America’s most convenient bank”: With over 1,200 branch locations, many of which open earlier and stay open later than its competitors, TD makes it easy for customers to get the service they need on their schedule. That exceptional service isn’t limited to TD’s brick-and-mortar locations: The bank also leverages data analytics to enhance its digital offerings and omnichannel experience.

- Capital One: Ranked #1 for customer satisfaction in the 2021 J.D. Power rankings, Capital One owes much of its success to its effort to continuously improve its digital banking experience. From offering digital wallet and contactless payment options to adding natural language process capabilities to its AI assistant to enabling customers to make digital deposits, Capital One is always looking for innovative ways to optimize CX.

The bank has also received attention for its recent rewards program partnerships with Walmart and Amazon, which enable customers to get more mileage out of their spending with some of their favorite eCommerce retailers.

- Ally Bank: Ally Bank has been a leader in the online retail banking space since its founding in 2009 thanks to its responsive, round-the-clock customer service, no minimum deposits or monthly maintenance fees, and interactive AI digital banking assistant, Ally Assist.

Similar to TD Bank, Ally has been open about its ongoing effort to enrich the customer experience through the use of data, including investing in cognitive computing to provide more realistic AI interactions and developing a 360-degree view of the customer for hyper-personalization.

- PNC: PNC has long prided itself on offering a hybrid banking experience, a vast network of branches (2,400, to be exact!), and digital money management services through its Virtual Wallet mobile app. PNC continuously looks for ways to optimize the customer experience in banking by marrying the physical with the digital, such as having its branches double as training centers for digital tools.

PNC also earns points for its attention to the little things. For example, each of the bank’s 18,000 ATMs enables customers to choose which denominations they’d like for their withdrawals, saving them the time and effort of making change.

7 Tips for Improving the Customer Experience in Banking

Looking to optimize your bank’s CX in 2023? Here are a few easy ways to get started:

- Map the banking customer journey. That might sound like a tall order given that the modern customer journey in the financial services sector is incredibly varied. However, identifying all of the potential paths customers can take and the touchpoints within each of those paths can help you appreciate how everything fits together. Once you’ve developed that end-to-end view, you can better understand what obstacles your customers typically encounter in their journeys, how to optimize each individual interaction, and how to create a more seamless, omnichannel banking customer experience.

- Assemble a dedicated CX team. Improving the customer experience in banking should always be a team effort — specifically, a cross-functional team effort. By calling upon the skills and expertise of leaders across multiple different departments, you can get unique perspectives and create a truly end-to-end financial services customer experience.

- Balance self-service with human interaction. Although self-service options and the convenience they offer have become table stakes for financial institutions, customers still want the option to speak to a live representative when they’re in need of assistance. Retaining top talent can be challenging in the current job market, but it will prove essential for banks looking to deliver quality service and exceed customer expectations.

- Establish strong feedback loops. When it comes to improving the customer experience in banking, your customers are your most valuable asset. Provide customers with an outlet through which they can share their thoughts and opinions about your current CX, the pain points they’re experiencing, and suggestions for improvement. Always remember to close your feedback loops by following up on every response you receive, whether that’s thanking a customer for their input or contacting them directly to help resolve any outstanding issues.

- Take an iterative approach to optimization. Not every CX initiative is going to be a rousing success, and that’s okay. Although it’s important to thoroughly test every CX-related product or service before releasing it to market, it’s equally important to treat each project as a learning opportunity. Even those that fall short of expectations can still reveal valuable insights for the next go-round.

- Keep the customer at the center of everything. Although it might seem obvious, you’d be surprised by how many institutions become so fixated on the idea of transformation solely for the sake of transformation that they lose sight of the customer in the process.

Data is, of course, an excellent resource when determining which improvements are most likely to appeal to customers, but no resource is more valuable than your customers, themselves. Maintain open lines of communication — remember those feedback loops! — and actually listen to what your customers have to say about what they want out of the CX. - Don’t bite off more than you can chew. As tempting it can be to kickstart multiple CX initiatives at once, transforming the customer experience in banking requires a measured approach. By focusing on one aspect of the customer experience and one project at a time, you can prevent things from getting out of hand, better manage your resources, make it easier to collaborate across functions, and scale over time.

Remember: Optimizing CX should be an iterative process; you can always focus on a different way to add value during your next project.

Hitachi Solutions: The Ideal Partner for Any Journey

The financial services industry is rapidly changing, shifting toward a model that prizes quality customer experiences over quality products. Are you able to keep up with the pace of change? How would your customers describe their experience with your organization and overall effort across channels?

With years of experience in helping banks, credit unions, and other financial institutions achieve digital transformation by harnessing the power of the Microsoft platform, Hitachi Solutions has seen — and done — it all. Our data science expertise and suite of industry-specific solutions make us the ideal partner for your journey.

We hope you found these banking customer experience trends helpful. Should you find yourself in need of assistance transforming your institution, just give us a call.

Frequently Asked Questions

Q: What is the customer experience in banking?

A: Customer experience in banking refers to a customer’s collective experience interacting with various touchpoints, including online banking systems, emails, call centers, online advertising, face-to-face interactions, and even social media.

Q: What do customers expect from a digital banking experience?

A: Generally speaking, customers want digital banking services to be convenient, easy to use, personalized, and secure. They also expect access to live assistance in situations where their needs exceed a bank’s digital banking capabilities.

Q: How can I measure banking customer satisfaction?

A: There are quite a few metrics that you can use to quantify customer satisfaction; the two most popular are Customer Satisfaction Score (CSAT) and Net Promoter Score (NPS). You can measure both CSAT and NPS by asking customers to rank how satisfied they are with their experience and how willing they’d be to recommend your brand via survey.

Q: How can I improve my bank’s customer experience?

A: In addition to reading up on the latest trends and investing in the right technology, you can also improve the customer experience in banking by:

- Assembling a dedicated CX team

- Establishing strong feedback loops

- Taking an iterative approach to optimization

- Keeping the customer at the heart of everything

- Being mindful not to bite off more than you can chew

Link: https://global.hitachi-solutions.com/blog/banking-customer-experience-trends/